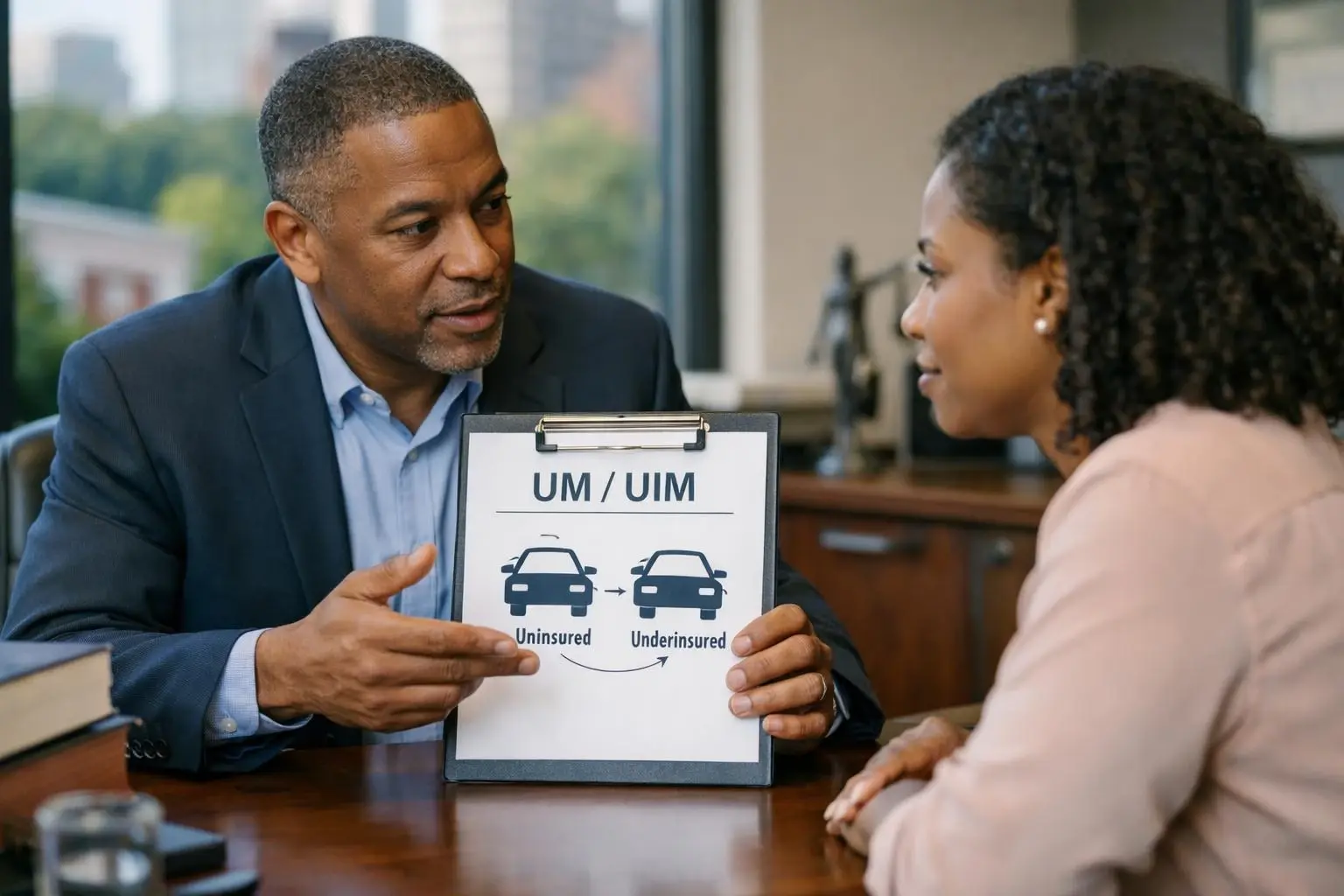

Understanding UM/UIM

UM/UIM means Uninsured Motorist (UM) and Underinsured Motorist (UIM) coverage. These coverages protect you and passengers in an accident. They help when the at-fault driver has little or no insurance to pay for damages.

Related glossary terms: Liability Insurance, Med Pay, Personal Injury Protection.

Georgia law requires drivers to have liability insurance. But not everyone follows the rules. Some only carry the minimum limits. These limits often aren't enough for serious injuries. UM/UIM coverage fills this gap. It lets your own insurance pay for medical bills, lost income. And other costs.

How UM/UIM Works?

UM coverage kicks in when the other driver has no insurance. UIM helps when their insurance isn't enough to cover your injuries. For example, say you're hit by a driver with only ,000 in coverage. But your medical bills total ,000. UIM can pay the extra ,000 if your limits are high enough.

Without UM/UIM, you might pay out-of-pocket for injuries. These injuries weren't even your fault.

How UM/UIM Works?

UM/UIM coverage is usually added to your auto policy. It's optional in most states. In Georgia, insurers must offer it. But you can say no in writing. If you choose it, you pick your coverage limits. These often match your liability limits.

For instance, if you have ,000 in liability coverage, you might pick ,000 for UM/UIM. After an accident, you file a claim with your own insurer. They step in where the at-fault driver's insurance falls short.

To use UM/UIM, you must prove the other driver was at fault. You also need to show their insurance wasn't enough. This might mean police reports, witness statements. And medical records. Your insurer will check the claim. They may negotiate the payout with you.

If you can't agree, you might need to take legal action. UM/UIM claims can get complex. Unlike simple liability claims, your own insurer handles these. They might try to pay less than you expect.

Why UM/UIM Matters?

UM/UIM coverage is critical. It protects you when the at-fault driver can't pay. Without it, you could face big bills for medical care, rehab. And lost wages. These costs hit even if the accident wasn't your fault.

In Georgia, about 12% of drivers have no insurance. Many more carry only the state minimum. That's ,000 per person and ,000 per accident. These limits run out fast in serious accidents. Victims have no other help unless they have UM/UIM.

UM/UIM also covers pain and suffering. Health insurance doesn't pay for these. This matters a lot in bad injuries. Long-term care and quality of life can suffer. UM/UIM keeps you from financial trouble after an accident.

When UM/UIM Matters Most?

UM/UIM coverage helps in several key situations. First, it matters in hit-and-run accidents. If the driver can't be found, UM steps in. There's no other insurance to cover your injuries.

Second, it helps when the at-fault driver's insurance is too low. This happens often in serious accidents. Think brain injuries, spinal damage. Or broken bones. UM/UIM covers the gap.

Third, it protects pedestrians, cyclists. And passengers. If an uninsured driver hits you, UM/UIM can pay. It also helps if you're in someone else's car.

UM/UIM is important if you lack health insurance. Or if your health plan has high deductibles. Without UM/UIM, you might pay medical costs yourself. Even if the accident wasn't your fault. It also covers passengers in your car. If an uninsured driver causes an accident, UM/UIM can help.

In Georgia, uninsured drivers are a big problem. UM/UIM coverage is a smart way to stay safe. It protects anyone who drives or rides in a vehicle.